A Mark, A Yen, A Buck or a Pound

A Mark, A Yen, A Buck or a Pound

Some stories about money

Sometimes when you’re a journalist, an editor comes to you and suggests a story or topic and you roll your eyes because—editors, what do they know?—but then you look into it and it turns out—hey, editors are smart! That’s the background to my latest round of stories, which are part of a personal finance package that TIME launched recently and that appears in the issue of TIME with Evan Gerskovich on the cover.

Why We’re Spending So Much Money

Banks Aren’t Doing Enough To Protect Customers from Scams

A few editors were interested in a package of personal finance stories, which made me initially cringe because the term “personal finance” has a sort of stigma to it. I think that I (and I most people) picture personal finance as advice about what you should and shouldn’t do with your money, and not only am I not particularly qualified to tell anyone that, but I find it a little repetitive. But I tried to think about personal finance stories as being about why we spend money and what we spend it on. If every story has money at its core, which I believe is true, there are money (many) stories that can be personal finance.

That led to the first story, Why We’re Spending So Much Money. I was interested in the idea that consumer spending is going absolutely bananas, even as economists say each month that it’s going to slow down (and then it doesn’t really). I started thinking about why people have been spending so much money since 2021 or so, and the pandemic revenge explanation didn’t quite cut it for me. Then I started thinking about what changed since 2021, and one thing that changed dramatically in the pandemic is people’s comfort sending money online, paying for things online, saving all their credit card info online.

It turns out that by 2023, 73% of consumers had paid for something through a website or browser on a phone or computer, according to a McKinsey survey, up from 46% in 2019. In this story, I argue that the rapid rise of fintech, or financial technology, has something to do with people spending so much money—more money than they realize. Fintech companies have made it so easy and fast to spend money that people are using Buy Now Pay Later, Venmo, and other services to spend, spend, spend. As a result, debt is growing. There are a few interesting studies that have looked into how people spend more on something if they’re using a credit card. They also spend more when the payment is quicker, so mobile payment has increased spending.

Interestingly, I talked to people in the story who got off all the apps, deleted their saved credit cards online, and “cash-stuffed”—put cash in envelopes for each of their monthly expenses, as a solution to getting out of debt. Their actions made me wonder if there’s a bigger backlash against fintech to come.

Speaking of fintech, the next story is about how many bank scams there are out there, and why banks should be doing more to stop them. Banks Aren’t Doing Enough to Protect Customers From Scams. This actually started as a story about an eighty-something year old woman who sent $67,000 to a scammer via wire transfer, but her case was more complicated than it initially looked. But there are many, many people out there who have been scammed into sending money on Zelle and Venmo, and because banks don’t have to compensate consumers for transactions they have authorized (even if they authorized them because they were scammed), many many people have lost lots of money.

I’d argue that as scammers get more sophisticated, consumers can’t reasonably be expected to know what is a scam and what isn’t—read some of the examples in the story and see if you agree with me—and that banks need to step up their fraud detection. This is a double-edged sword, because it is VERY annoying when a bank won’t let a legitimate transaction go through, but it turns out there is a lot of technology they could be using to catch scammers, but are not because it’s pretty expensive.

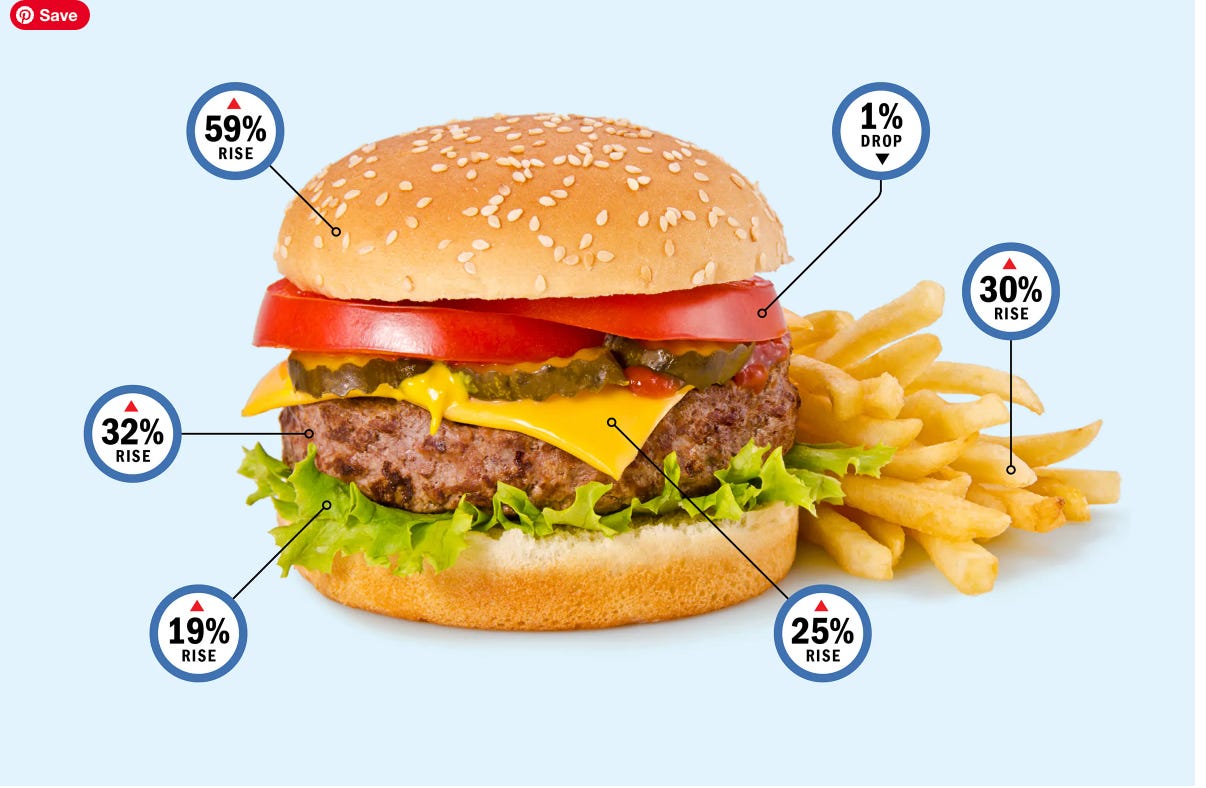

Lastly, I looked into the many factors that have driven up the cost of a cheeseburger and fries since 2019. Why a Burger Costs More. The good news is that inflation is slowing. The bad news is that farmers say that beef and dairy might be even more expensive this year because of various drought and other factors. Nuts and berries, here I come.

These stories, one more time:

Why We’re Spending So Much Money

Banks Aren’t Doing Enough To Protect Customers from Scams

BFAT, Books to Fall Asleep To

Fun reveal: in my spare time I am trying to write a musical (!?) that is set in 1920. I have been reading and listening to a lot about the year 1920 and President Warren G. Harding for reasons that will become clear when my musical debuts on Broadway in the year 2040. If you are interested in the year 1920, and why shouldn’t you be?, I’d recommend the audiobook 1920: The Year That Made the Decade Roar, by Eric Burns. It turns out 1920 was a pretty bonkers year, with Prohibition bumping off, women finally getting the right to vote, and Charles Ponzi launching his financial scheme, sucking in lots of investors, and then getting caught. Now there’s a guy who needed to read some personal finance journalism.